Author: Valentijn van Nieuwenhuijzen, CIO NN Investment Partners

Investor fears rather than tangible risks appear to be currently driving investor behaviour. We see this as a reason to move risky assets to a neutral stance.

Correct on correction

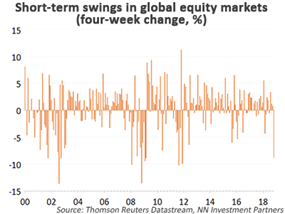

Markets are on the move again, and in a pretty impressive way. A combination of rising risk aversion, lingering trade worries and disappointing European data led to extended negative market sentiment last week, despite another strong US earnings season. For global equity markets, the 8% decline in October will be one of the biggest monthly moves in recent history (see graph). Market sentiment was also very negative during the volatility shock in February of this year, and when China’s policy regime shift and falling commodity prices in 2015 and 2016 caused substantial worries, but the equity market corrections over a four-week period were mostly limited to 4%-6%.

Markets fell more sharply during the heights of the euro crisis in 2010-12, the fallout of the credit crisis in 2008-09, the accountancy scandals in the summer of 2002 and after the September 11 terrorist attacks in 2001. Still, since the start of this century there have been only 10 corrections in equities similar to or larger than that of the last four weeks. In almost all of these periods, some shock to the system, systematic crisis or sharp economic slowdown was taking place. There are more than enough worries about the economic and political outlook today, but it seems hard to argue that systematic fragility of the business cycle is comparable to previous crisis periods.

There are a couple of reasons why the macroeconomic picture does not justify the recent market weakness. First, the underlying fundamentals for domestic demand in developed markets remain relatively firm. Labour markets continue to tighten and wage growth is picking up. Also, business confidence continues to be pretty firm, which in combination with improved profit margins and a low investment-to-output ratio should stimulate capex demand. Furthermore, the balance between credit demand and supply remains conducive to a further pick-up in credit growth, and fiscal policy is set to remain neutral to stimulative. Going into 2019, the effect of US fiscal stimulus will gradually wane, and the effects of past Fed tightening should also start to be felt. This should produce a moderate slowdown in US growth, but Europe should emerge from its current soft patch on the back of the aforementioned fundamentals and continue to show above-trend growth for most of next year. Bear in mind that there is still some slack and pent-up demand for capital goods in Euroland, and ECB policy will not be tightened in the near future.

Second, after the correction of the past quarters, risks in emerging markets are more balanced than they were. The fundamentally weakest countries have already been forced into substantial growth adjustment, which creates room for a recovery. So far, markets have been disappointed with the level of Chinese policy stimulus, but this does not mean that China will not deliver. The main difference with earlier cycles is that China is now focusing more on household consumption than fixed investment. This makes it more difficult to predict when the Chinese stimulus will kick in to offset the negative impact from US tariffs.

Third, global trade risks narrowed down to the China-US axis in the autumn. It became clear that the big underlying theme is the competition for global leadership between these two countries. This suggests that China-US tensions will remain a chronic theme for markets. We could also see negative effects on business confidence and financial market sentiment in certain periods. Still, with the trade story mostly remaining confined to the China-US axis and not spreading to other major trading partners like Europe, Japan, Canada or Mexico, it will be an occasional source of volatility, but not a derailing force for the global business cycle.

Comparing the market evolution with the evidence and outlook on the global economy strongly suggests that a short-term overshoot in negative sentiment has taken place. Global growth is consolidating, and cyclical and political risks are certainly around, but a historical perspective on the shape of the market correction suggests that investor fears rather than tangible macro or earnings risks are currently driving investor behaviour. We do not see this as a reason to become positive again on risky assets, but certainly as a trigger to tactically unwind our defensive tilt in asset allocation and move risky assets to a neutral stance. And when the market dust settles we will consider the next move, but let’s wait until that happens.